Strategy

Private Banks' Onboarding Limitations Revealed â And How To Fix Them

Client onboarding in private banking is riddled with inefficiencies â not just for high-risk clients but across the board â according to a study.Â

While it can take several months to onboard clients deemed to be high risk, data shows that customers lower down the risk spectrum, who make up 60 per cent of total private banking clients across the industry, often face similar frustrations, an Asian-focused Singapore-focused report has found.

At the root of the issue, arguably, is a fragmented strategy. Disparities across process, tools, and governance have left onboarding capabilities misaligned with what clients expect. Instead of a streamlined, risk-calibrated approach, many banks struggle with a one-size-fits-all model that frustrates clients and hampers operational efficiency.

Embracing modern technology to ease the frictions of this onboarding and aligning the process to client expectations is important, particularly as thereâs a talent crunch for banks in handling the processes needed to get new clients through the door. The stakes are high as private banks compete for wallet share, with clients in Asia maintaining an average of three private banking relationships.

Sia, a global management consultancy, argues that there is a need to strategically align the onboarding function across the entire value chain â from relationship managers and onboarding teams to compliance and operations. This orchestration is essential to drive efficiency and create a seamless client experience, it says.

Sia has issued a Private Banking Client Onboarding

Benchmark study, based on data from 15 banks in Singapore.

(Their identities were not disclosed.)

â

Siaâs report was explained to WealthBriefingAsia in a

recent call by Hassan Naveed, who is senior manager, private

banking and wealth management, and David Hollander, head of

financial services, APAC at Sia. The firm, Hassan said, conducted

deep-dive discovery workshops with more than 70 private

banking professionals from 15 private banks to gather

industry-wide trends, and build the diagnostic using more than

1,200 data points across KYC, AML, source of wealth and

other processes, engaged in a range of discussion workshops

with banks, exploring their know your client (KYC), anti-money

laundering (AML) and onboarding processes.

The study highlights trends on adoption of e-signatures, maturity curve across name screening, training and retention of talent, and varied approaches for source of wealth corroboration.

(For more information on Sia, see here.)

Navigation

Globally, private banks and wealth managers must navigate between

regulatory pressure, an increasingly competitive landscape, and

heightened client expectations for a faster turnaround driven by

the digital wave. If it takes a long time to onboard clients,

some people will quit and try for an easier experience

(hopefully) somewhere else. A variety of studies show

that long onboarding times are

a headache.

Singapore is also feeling the regulatory heat, amidst memories of a recent prominent money laundering scandal that has prompted authorities to be even more vigilant. (See a related story.)

And at a time when the worldâs financial services industry is being confronted with the opportunities â and competitive challenges â of AI, the way that technology intersects with the task of onboarding is in the limelight.

âOnboarding is the first impression the client will have of the bank. Expectations from client and regulators are evolving on a regular basis, however, the private banking industry has been rather conservative and very admin heavy and there is a strong push now to reevaluate the approach starting from client onboarding. The banks which have the smoothest onboarding will be the winners in the long run,â Hassan said.

WBA asked Hollander what was the main message that should come out of this benchmark?

âThere is no one-size-fits-all approach to succeed in onboarding. It is about strategising your investments based on your volumes, client focus, the current tech infrastructure, and the risk-management approach. The private banks can learn from the industry best practices and adapt them in the context of the challenges they are facing,â he said. âOnboarding has become a key differentiator in Singaporeâs highly competitive market, as new entrants â from Middle Eastern firms to digital players â seek a share of the pie.â

Digital engagement

The report notes, for example, that only 13 per cent of banks can

onboard a client fully digitally and the rest are pushing towards

a hybrid model to move away from the pure pen and paper

exercise.

And the number of forms used by banks varies widely, with one bank requiring almost 20, and taking almost 20 signatures, while at the other end of the scale, one bank appeared to require only five signatures and about 10 forms. According to the report, an increasing number of private banks have begun embedding forms under a single T&C to reduce signatures required.

Another part of the report notes the average amount of time it takes to onboard a person based on whether they are high risk, medium risk or low risk. In the different clusters of results, it shows that six banks took two to four weeks to onboard a low-risk client; three took four to six weeks and four took six to eight weeks. At the high-risk end, three banks took more than six months, six took two to six months, and five took six to eight weeks. It is key to note that the average onboarding duration for low-risk clients is four to six weeks, with many banks pushing to onboard this client segment within the two-week window.

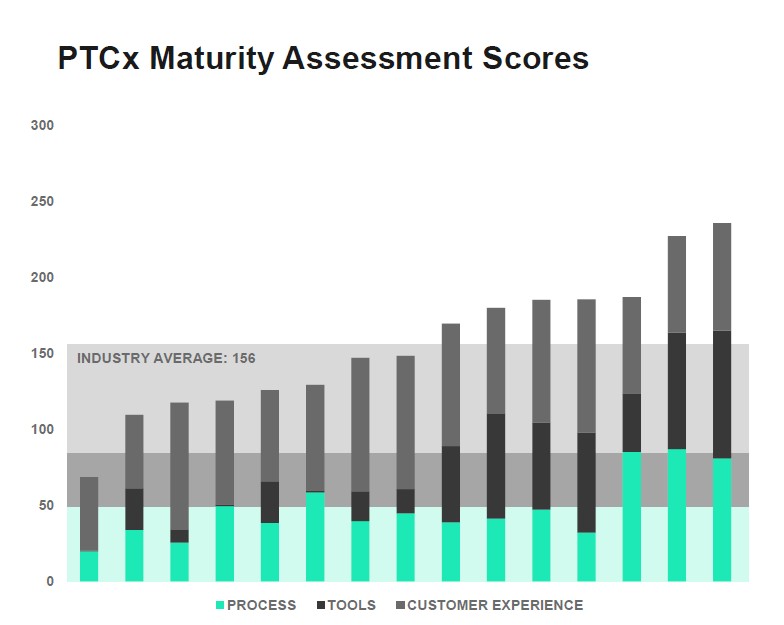

Sia also conducted a âmaturity assessmentâ to see how well banks

in the study apply tools, processes and manage the customer

experience, looking across a range of measures to come up with a

300-point scale. It found, for example, that banks that score

highly on the use of tools frequently achieve strong client

experience ratings, although this link does not hold true when

looking at processes. It noted that some banks, even if they rely

on manual processes and have limited tools, can achieve high

client experience results by using large teams to make the

process as fast as possible.

Out of the 15 banks assessed, seven banks scored above the industry average of 156, demonstrating stronger onboarding maturity. The highest-scoring bank achieved 236 points, significantly outperforming its peers, while the lowest-ranked bank recorded just 69 points. Overall, half of all banks studied fell below the industry benchmark, highlighting the need for strategic improvements in process, tools, and customer experience.

Last year, Sia hosted an event to present their report to industry leaders. They are now conducting deep-dive exercises with various private banks to re-strategise ongoing initiatives based on the benchmark's findings.

Picture of the Sia team at a recent industry event, showing David Hollander (far left) and Hassan Naveed (far right).