The Japanese stock market hasn’t escaped the broader stock market rout of 2022 but, as wealth managers know, the details are what counts. The Japanese market has had its problems over the years but this news service notices how the case for it continues to made. In this article, looks at the “growth” versus “value” debate in the equities sphere. The firm says much of this debate misses a point.

The author of this article is Satoshi Marui, portfolio manager of the SuMi TRUST Japan Small-Cap fund. The editors of this news service are pleased to share these views; the usual editorial disclaimers apply. Jump into the conversation! Email tom.burroughes@wealthbriefing.com

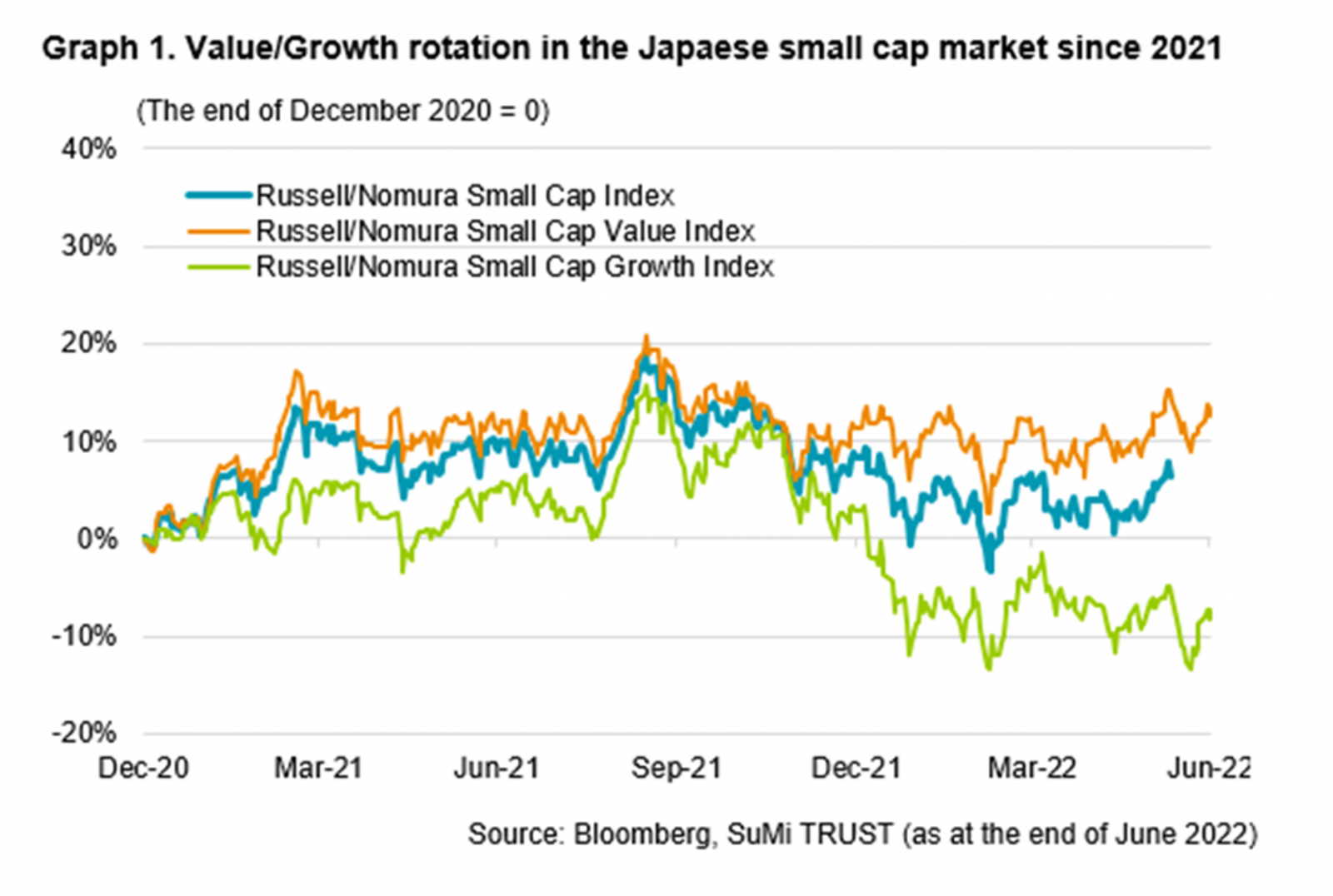

The value rotation is foremost in investors’ minds, but when it comes to Japanese small-caps there are strong reasons to keep an open mind and invest in both value and growth stocks. Companies with long-term earnings growth potential, whether they are in the growth or value bucket, remain the best bet for investors. The shift to value isn’t based on changing company fundamentals and represents an overreaction.

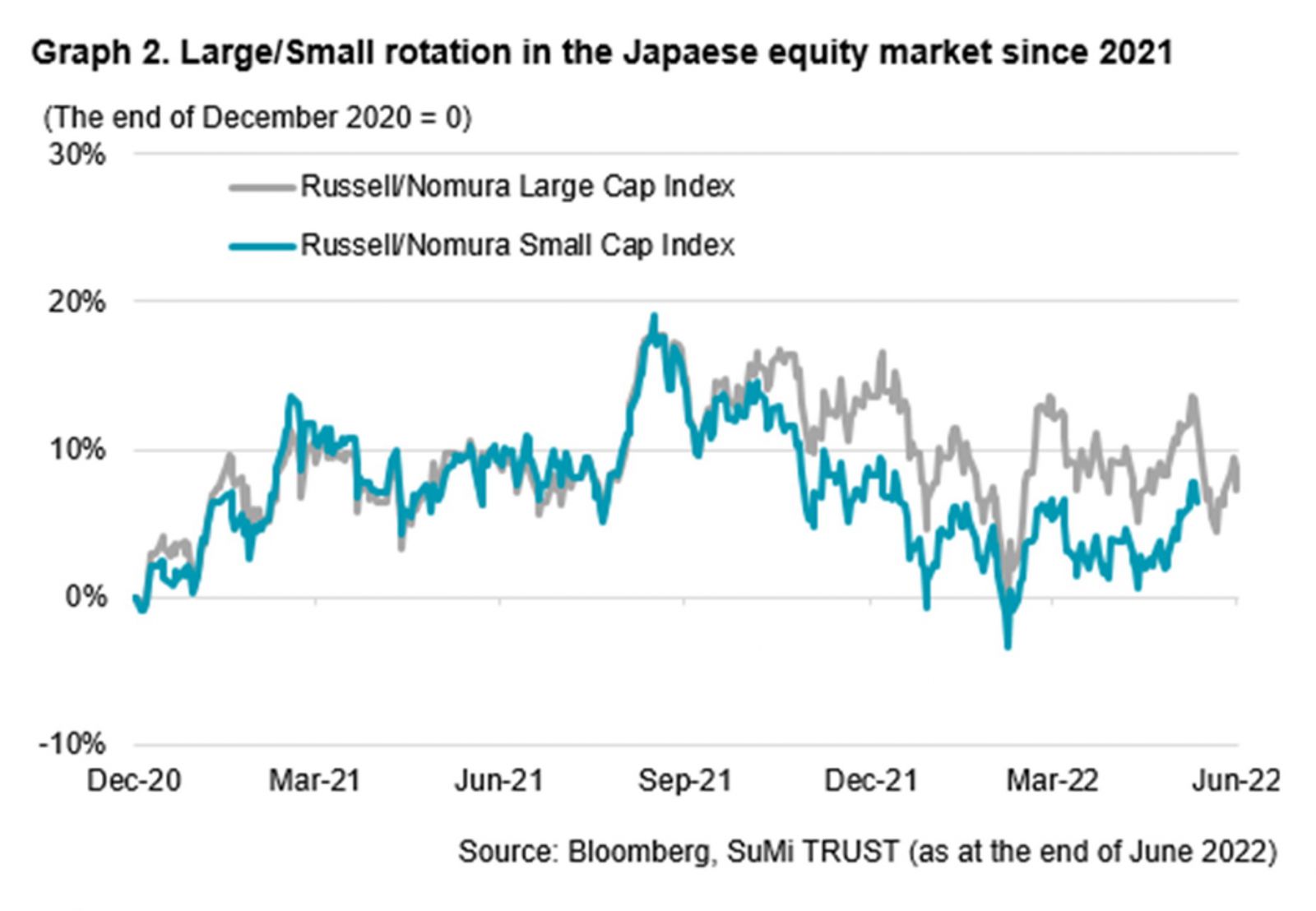

Since December 2021, large-cap value stocks in Japan have outperformed. Growth stocks have lagged and, as the proportion is greater in the small-cap than large-cap space, small caps have underperformed, and have been sold off significantly in the Japanese stock market. Yet all is not quite what it seems.

For a start, one might ask why Japan is undergoing a value rotation. The principal rationale given by investors is rising inflation and interest rates, which have a greater impact on companies valued for their future earnings' growth rather than present income.

Yet Japan does not suffer from inflation to anything like the extent of the US or Europe; consumer price inflation has risen to over 8 per cent in the UK and the US, whilst Japan’s was only 2.5 per cent in May. Indeed, the Bank of Japan is considering sticking with its easy monetary policy, in stark contrast to the tightening of monetary policy being initiated by other central banks to try to curb inflation.

Second, Japan is in the process of a profound technological transformation. In many ways, the nation lags behind other developed countries in its use of software and online systems. Japan excels at electrical hardware but scores poorly when it comes to digitalisation. Many smaller companies, along with the government, are trying to change this. Some of the most innovative names in the space that generate strong profits and use AI and online processes to create efficiencies have suffered big share price declines despite having persistently strong fundamentals and long-term earnings growth potential.

Two great examples are Solasto, a medical administration company, and Syuppin, a website selling secondhand watches and cameras. Solasto will help to streamline Japanese healthcare as it provides a solution to the sheer volume of paperwork still prevalent in its administrative system. This gives the company an obvious long-term advantage, yet its share price has fallen by 50 per cent since September 2021. Syuppin provides a sense of community for Japanese consumers interested in photography.

It not only sells cameras but also allows fellow hobbyists to connect, form relationships and groups, and produces online advice. Structural factors in the Japanese economy make this concept quite unique in Japan, as opposed to the US and Europe. This, combined with the AI-based machine learning, Syuppin uses for the purpose of one-to-one marketing content, gives the company and others like it strong tailwinds and long-term earnings growth potential. It would be a mistake to overlook them because of interest rate decisions in the US and Europe.

That is not to say that there aren’t opportunities in value stocks and those hybrid stocks that are hard to categorise, such as Mirait Holdings, a telecommunications engineering and architectural firm, and Furuya Metal, which manufactures products using platinum-group metals (such as platinum and iridium). Mirait Holdings is classed as a value stock, but Furuya Metals is better described as a hybrid. Its current price/equity ratio suggests that it is a value stock while its long-term earnings potential suggests it is a growth stock.

Even though they can be classed slightly differently, they are nonetheless both good examples of small-cap non-growth stocks with strong fundamentals and momentum but with P/E ratios that are slightly depressed.

Investors in Japan need to be open to long-term investment in all kinds of small-cap companies rather than just take the current situation of rising inflation and interest rates abroad as a cue to dump growth stocks for value. A market where only value stocks are being bought will not last for a long time, and it would be unwise to invest based on the assumption that it will.

In the future the binary distinction between value and growth stocks will begin to erode, as the market will focus more on companies with long-term earnings growth potential. Companies that provide new technologies which can solve social issues or use technologies to transform their own business models and services for the better are ultimately the stocks that will provide the best returns in the long-term. This trend is one that has been accelerated by the pandemic, and it is not one that is going anywhere.

Indeed, we are only going to see more and more companies, regardless of their classification as growth, value or hybrid stocks, using new technology in more sectors as time goes on and as the impact of Covid-19 fades away. Therefore, it would be a mistake to switch to value stocks because of short-term factors. Irrespective of whether a stock is in the value or growth camp, it is strong fundamentals and technological innovation that make a company a good investment.